There’s never one way to become wealthy, but there are consistent habits among self-made wealthy people that may put you in a position to achieve financial

Financial Planning, Master Your Money and Mindset, Media, Podcasts

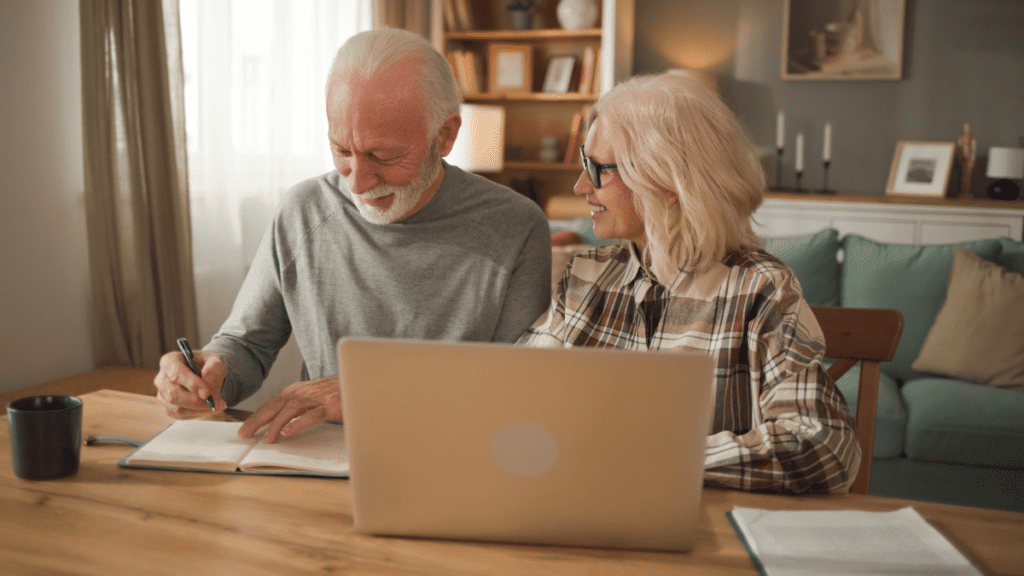

We’re going to walk through exactly how to do a retirement plan check-up and make you question: Have you checked your retirement

Financial essentials at your fingertips. Delivered to your inbox monthly.

Barnum is committed to protecting and respecting your privacy. By clicking Subscribe below, you agree to receive all Marketing updates via email. You can unsubscribe from these communications at any time. For more information on how to unsubscribe, our privacy practices, and how we are committed to protecting and respecting your privacy, please review our Privacy Policy.

By clicking Subscribe above, you consent to allow Barnum to store and process the personal information submitted above to provide you the content requested.

Secure Form

Americans In The Workplace Study

This comprehensive study dives into the evolving financial behaviors of American workers across a variety of factors, including generational, household income, gender, and employment status and more !!